By Steve Martin

First, the good news: you will probably live much longer than you think: maybe to Age 100 – or beyond. But here’s the bad news: unless you’ve already amassed a small fortune and have a plan for preserving it to last those 100 years, you’re going to have to figure out a way to pay for living that long.

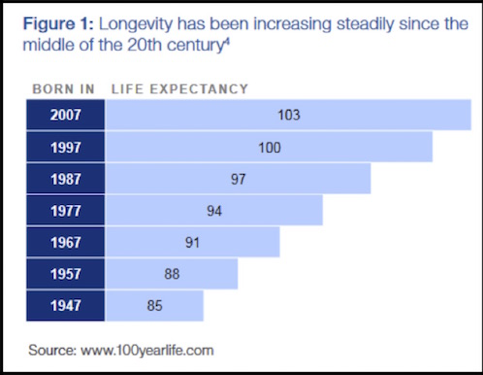

Consider this forecast done by the World Economic Forum:

The ages shown on this chart are median life expectancies, which means that half the people in each category shown will live longer than the median, and that’s not considering the life-extending medical breakthroughs that may happen in just the next decade. It’s quite possible that some of our younger Millennials today will see their lives span three different centuries!

So if half of the present population will live to Age 80 or 90 – or even Age 100, the present “standard” of retiring between the ages of 60 and 70 isn’t going to be sustainable. If current trends continue, according to the World Economic Forum, the ratio of active workers to retirees (also known as the “dependency ratio”) in developed markets will shrink to 2:1 (down from 8:1 today). Given this declining dependency ratio and the likely rise in our longevity, public and private sector employers, as well as the policy-makers in Washington need to find ways to enable older workers to extend their working careers as much as possible. That may not be what those of us over 50 and still working want to hear, but the reality is, if we are going to be living longer, it’s likely we will need to be working longer to pay for it.

So, if you think you will live for 100 years and you want to make the most of it, here are some retirement planning steps to consider:

- Have a financial planner prepare a retirement forecast for you, assuming you will live that long and do it now. This will help you examine what variables you can control in order to have a successful retirement. Plan to re-visit that forecast annually, and make adjustments along the way according to their recommendations. This should include a savings and/or investment plan, a hard look at your living expenses, and a plan to manage for the risks you may encounter along the way.

- Mentally plan to work longer than you thought you might – even considering part-time work. The benefits of this are many, not the least of which is that working keeps you engaged with others, and if you are still earning money, you are likely not spending (or spending as much) from your retirement “nest egg” too soon. Note: This may require you to develop new skills or polish existing ones in order to stay relevant in the workplace, so mentally plan for that, too!

- Stay as healthy as possible for as long as possible. This may sound like a silly suggestion, but I believe the single best investment we can make for our retirement is to make healthy lifestyle choices: diet, exercise, stress-reduction techniques, regular wellness check-ups, etc. Of course, there are certain health circumstances beyond our control (see my future article about planning for that), but with adult obesity at epidemic proportions dramatically increasing the cost of our healthcare, there is a lot we can

- Before you sell your business or turn in that resignation letter to your employer, consult your financial planner again – to make sure your retirement forecast still works. Have your financial planner help you create a retirement spending plan, so you know where your sources of cash flow will come from, and how sustainable they are. If something doesn’t look quite right with this plan, you will still have time to make adjustments before you “pull that trigger.”

- Once retired, have a plan for what you’ll do then, too. Whether it be playing golf or tennis, volunteer work, joining clubs, taking classes for fun, or some combination of all of these, if you plan to stay engaged, you’ll likely live longer, and the quality of that life will surely be enhanced.

None of us truly know how long we have to live. But chances are, it will be longer than we think. Therefore, it’s no time like the present to start getting prepared for that. If you’d like help creating or re-visiting your retirement plan with “100 years to live,” please give our offices a call.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Investing involves risk including loss of principal. No strategy assures success or protects against loss.